Buying two prop firm evaluations sounds simple enough.

You pass both, scale faster, and get access to more funded capital. That is the dream, right?

But there is a catch. The way you trade those two accounts matters a lot. If you copy every trade across both accounts from day one, you are not really giving yourself two independent chances. You are tying both accounts to the exact same trade sequence.

That can feel amazing during a winning streak. It can also wipe out both evaluations during the same bad patch.

At PropFirmWizard, we tested different prop firm account rotation methods to see how they affect the chance of getting at least one account passed. The goal was not to magically improve the trading strategy itself. The goal was to reduce account correlation, control path dependency, and avoid letting one bad run take out every account at the same time.

The results were clear:

- Mirrored or stacked accounts had a 45.5% chance of at least one account passing.

- A 3-day lagged start raised that to 55.3%.

- A 3-day lagged start with terminal staggering raised it again to 61.6%.

- Alternate days produced the highest at-least-one-pass rate at 70.7%, but it was much slower.

That last point matters. The best prop firm evaluation strategy is not always the one with the highest pass probability on paper. You also have to think about time, throughput, rules, risk, and how quickly you can get capital working.

Let's break down how account rotation works, what the data showed, and how you can use it when scaling through prop firm challenges.

What Is Prop Firm Account Rotation?

Prop firm account rotation is the process of deciding which evaluation account gets traded on each valid trade setup.

Instead of automatically copying every trade across every account, you create rules for when each account is active. For example, you might:

- Trade both accounts at the same time.

- Trade Account A one day and Account B the next.

- Start Account A first, then start Account B a few trading days later.

- Trade only the account with the lowest remaining drawdown buffer when risk gets tight.

The point is not to avoid losses. Losses are part of trading. The point is to avoid stacking the same loss across every account when you do not have to.

This is especially important in prop firm challenges because evaluations are path dependent. You can have a profitable strategy over 500 trades and still fail a challenge if the wrong losing streak happens early.

That is where rotation helps. It does not change your edge, but it can change how that edge is distributed across accounts.

The Research Setup

The test compared several account rotation policies using Monte Carlo simulation.

The pair-level model used 50,000 Monte Carlo paths per policy. The evaluation model used a $3,000 profit target and a $2,000 end-of-day trailing drawdown. The sizing model used $1,000 normal risk, reduced risk when drawdown buffer became tight, and stopped initiating new trades below a $500 buffer.

The source strategy data covered:

- 1,112 logical trades

- 618 active trade days

- Date range from January 31, 2023 to March 24, 2026

- 81.9% trade win rate

- 69.9% daily win rate

- $78,326 total modeled PnL

- 1.41 profit factor

- $70 average trade

- $294 average winner

- $944 average loser

One important note: the headline metric is the chance that at least one of two accounts passes. Individual account pass rate barely changed across policies, staying around 45.5% to 46.0%.

That distinction is huge.

Account rotation did not make the trading strategy more profitable. It reduced correlation between Account A and Account B. In plain English, it helped prevent both accounts from living and dying on the exact same sequence of trades.

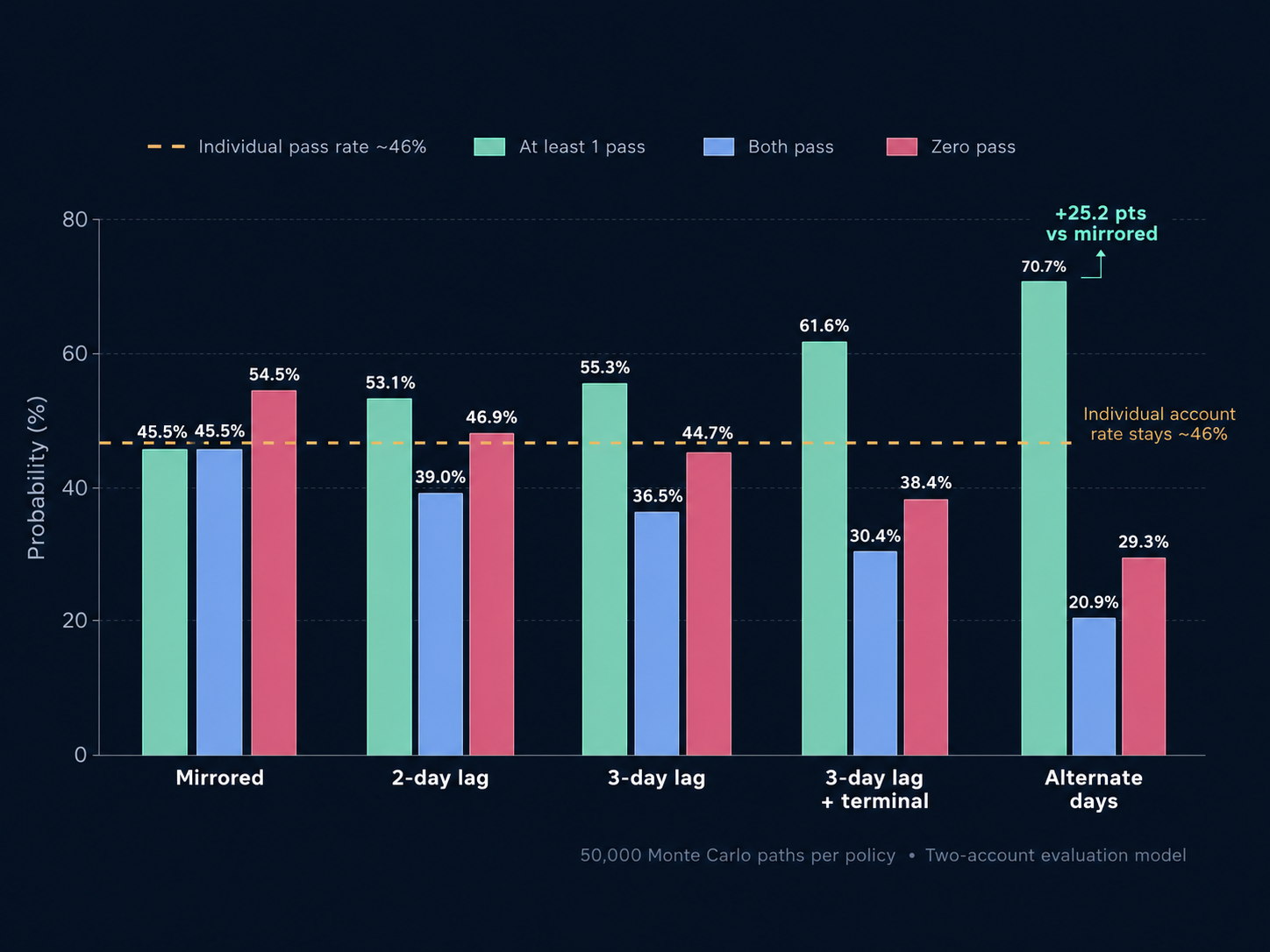

Rotation Results at a Glance

Here is the clean version of the pair-level results.

| Rotation Policy | Individual Account Pass Rate | At Least 1 Pass | Both Pass | Zero Pass | Avg First Pass Day |

|---|---|---|---|---|---|

| Mirrored / stacked start | 45.5% | 45.5% | 45.5% | 54.5% | 9.7 |

| Lagged start, 2 days | 46.0% | 53.1% | 39.0% | 46.9% | 9.9 |

| Lagged start, 3 days | 45.9% | 55.3% | 36.5% | 44.7% | 10.2 |

| Lagged start, 3 days + terminal stagger | 46.0% | 61.6% | 30.4% | 38.4% | 11.2 |

| Alternate days | 45.8% | 70.7% | 20.9% | 29.3% | 17.6 |

"Days" here means active strategy or opportunity days, not necessarily calendar days.

The trade-off is pretty clear. The more you separate the accounts, the lower your chance of passing both at the same time. But your chance of passing at least one account goes up because you are less likely to lose both accounts together.

That is the whole game.

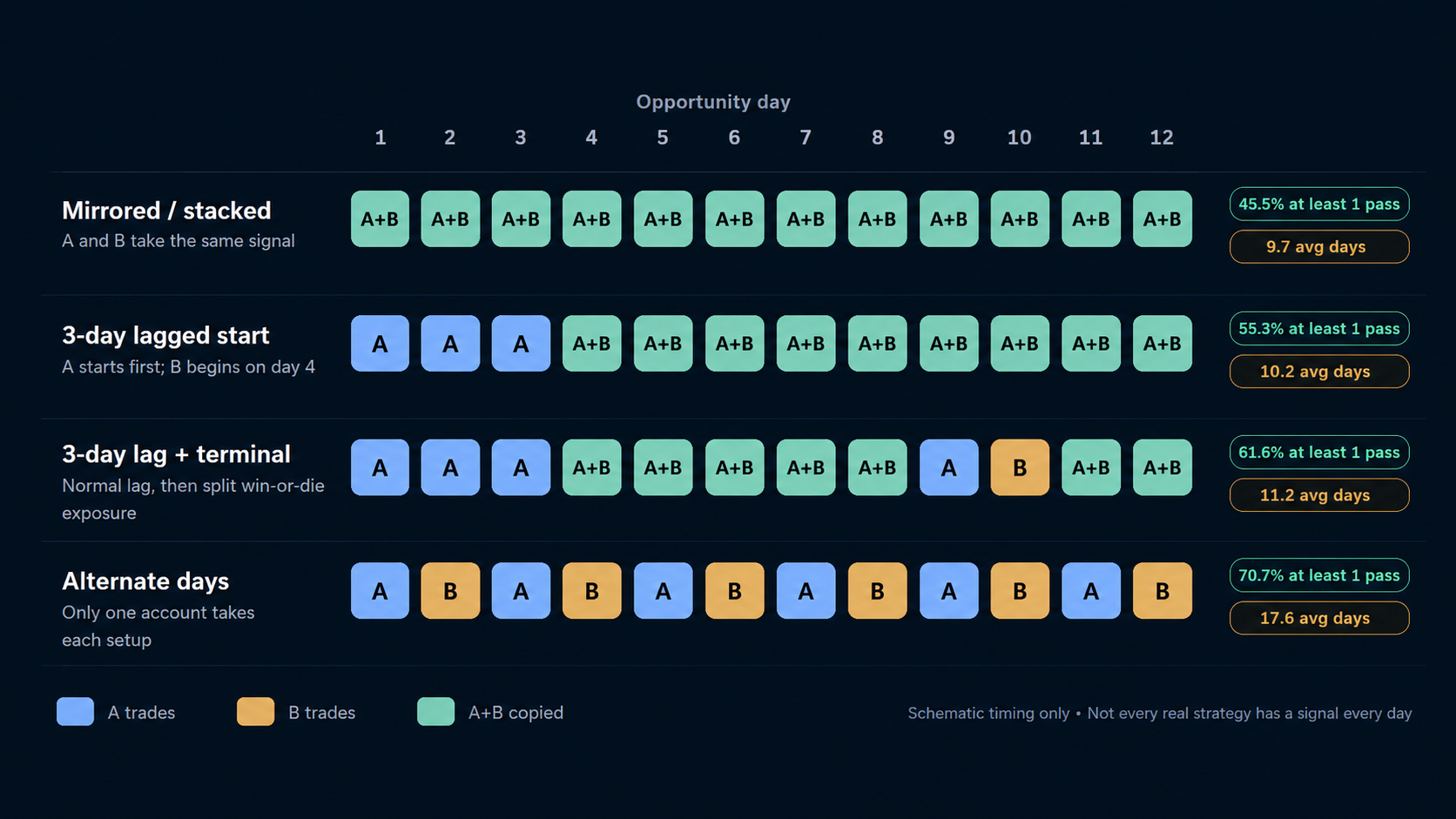

Strategy 1: Stacked Accounts

Stacked accounts are the easiest to understand. You buy two prop firm evaluations and copy every trade across both accounts from the start.

If Account A takes a long trade, Account B takes the same long trade. If Account A wins, Account B wins. If Account A loses, Account B loses.

This approach is attractive because it gives you maximum upside when things go well. One strong sequence can push both accounts toward the profit target quickly. In the test, mirrored accounts had the fastest average first pass day at 9.7 opportunity days.

But stacked accounts also had a major weakness. The at-least-one-pass rate was only 45.5%, exactly the same as the both-pass rate. That is because both accounts were almost perfectly tied together.

You were not really getting two separate shots. You were getting one shot with double exposure.

That may be fine for experienced traders who understand the risk and are intentionally trying to scale aggressively. But for most traders trying to build consistency, stacked accounts can be brutal. A few early losses can put both accounts near failure before the edge has enough time to play out.

Stacked accounts are best when:

- You have a high-conviction strategy.

- You are comfortable with both accounts failing together.

- You care more about speed than survival.

- You are not relying on one account passing to fund future attempts.

For newer traders, or traders still validating a strategy, stacking every trade across multiple accounts is usually too correlated.

Strategy 2: Alternate Days

The alternate-days approach is the opposite of stacked accounts.

Instead of trading both accounts on the same setup, you rotate exposure. Account A gets one valid opportunity, Account B gets the next, then Account A again, and so on.

This reduces correlation dramatically. In the test, Account A and Account B correlation dropped to 0.00. That is why alternate days produced the highest chance of at least one account passing at 70.7%.

That is a big jump from the 45.5% at-least-one-pass rate for mirrored accounts.

The downside is speed. Alternate days had an average first pass day of 17.6 opportunity days, compared with 9.7 for mirrored accounts and 10.2 for the plain 3-day lag.

So, alternate days are safer in one sense, but slower in another. You are spreading your edge across accounts instead of pushing both accounts forward at the same time.

Alternate days can make sense when:

- Your main goal is getting at least one account passed.

- You want to avoid losing multiple accounts on the same bad trade.

- You are patient with slower challenge completion.

- You have limited budget for resets or new evaluations.

- You are trying to reduce emotional swings from all-or-nothing outcomes.

The key downside is opportunity cost. If your strategy is strong, rotating every trade may reduce throughput. You might protect against correlation, but you may also take longer to actually get funded.

Strategy 3: Lagged Start

The lagged-start approach sits in the middle.

Instead of starting both accounts on day one, you begin Account A first. Then, after a set number of opportunity days, you begin Account B.

In the research, the 3-day lagged start was the best middle-ground policy. It raised the chance of at least one account passing from 45.5% to 55.3%, while the average first pass day moved only from 9.7 to 10.2 opportunity days.

That is a strong trade-off.

You give up a little bit of pure speed, but you reduce the chance that both accounts get damaged by the exact same early sequence. If the first few trades are bad, Account B has not taken all of that damage. If the first few trades are good, Account A is already moving toward the profit target before Account B starts.

The 3-day lag works because it reduces some path dependency without completely slowing down the account pipeline.

It is not the highest probability method. Alternate days had the highest at-least-one-pass rate. But the 3-day lag is more balanced because it preserves much more speed.

A lagged start can make sense when:

- You want a better chance of at least one account passing.

- You do not want to cut throughput too aggressively.

- You are trading a strategy with frequent enough setups.

- You want a simple rule that is easy to follow.

- You are building a repeatable evaluation process.

For many traders, this is the practical sweet spot.

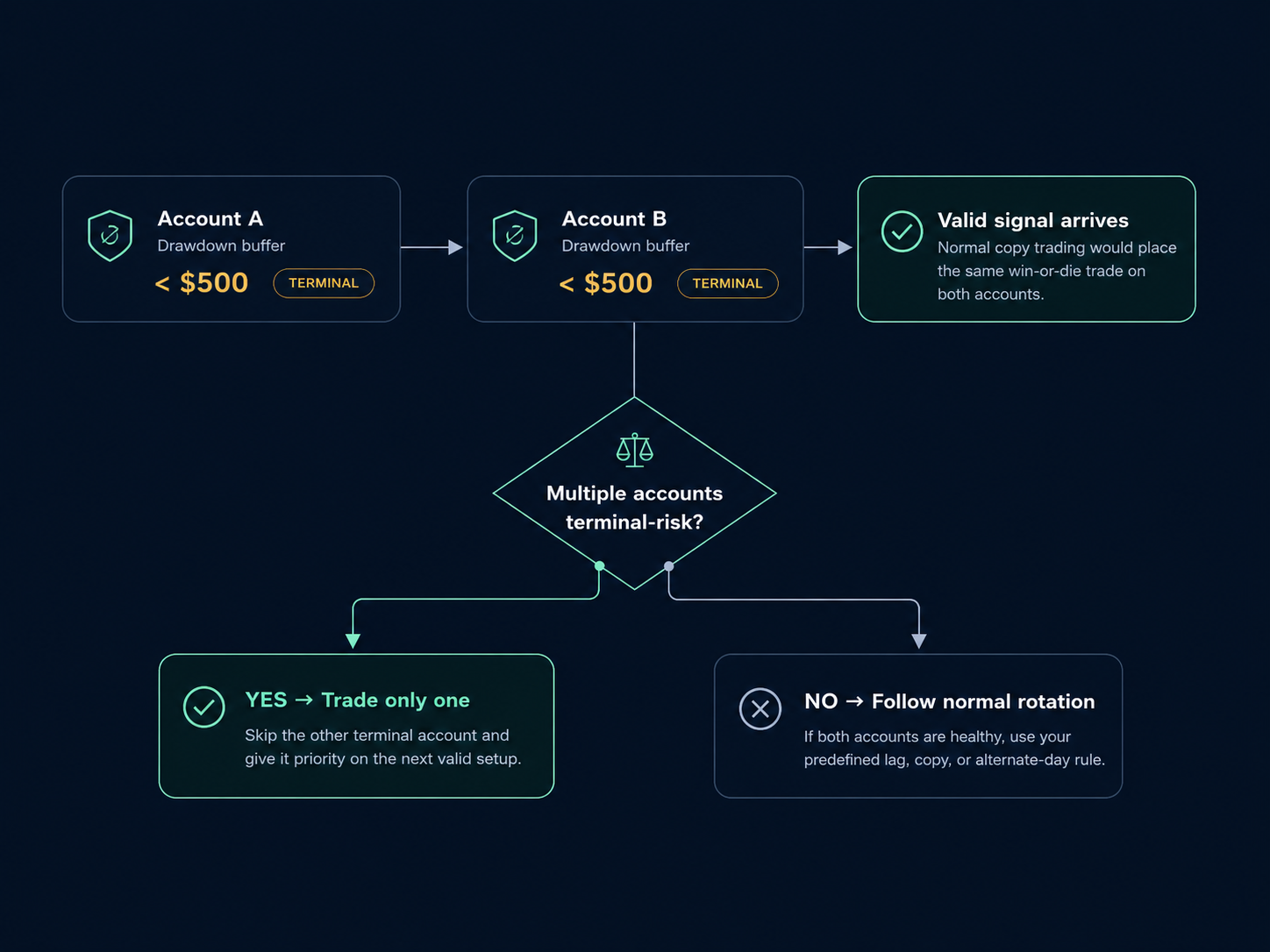

Strategy 4: Terminal Staggering

Terminal staggering is a risk-control rule that applies when one or more accounts are close to failure.

The rule is simple:

If multiple active accounts are in a "win-or-die" state on the same signal, trade only one terminal-risk account and prioritize the skipped account on the next opportunity.

In plain English, if both accounts only have enough drawdown buffer left for one more real trade, do not take the same trade on both. Trade one account. If it loses, you still have another account alive for the next valid setup.

This rule takes the best part of alternate-day rotation and applies it only when the stakes are highest.

In the research, adding terminal staggering to the 3-day lag raised the at-least-one-pass rate from 55.3% to 61.6%. The average first pass day moved from 10.2 to 11.2 opportunity days.

So, you gained 6.3 percentage points in at-least-one-pass probability compared with the plain 3-day lag, while only adding about one opportunity day to average first pass time.

Compared with mirrored accounts, the 3-day lag plus terminal stagger improved the at-least-one-pass rate by 16.1 percentage points.

That is the kind of rule traders often miss. Most people think only about entries, exits, and risk per trade. But in prop firm evaluations, account state matters too. A trade that is reasonable for one account may not be reasonable for another account if the second account is one loss away from failing.

Why Rotation Improves Outcomes Without Improving the Strategy

This is the most important concept in the whole article.

Account rotation does not make your entries better. It does not improve your win rate. It does not change your average trade.

What it changes is account correlation.

When two accounts take the same trades, their outcomes are tied together. If one passes, both may pass. If one fails, both may fail.

When accounts are rotated, they experience different parts of the trade sequence. One account might skip a losing day. Another might catch a winning streak. Over many simulations, this lowers the chance that both accounts fail together.

That is why the expected number of passes across two accounts stayed around 0.91 to 0.92 for every policy. Rotation mainly changed variance and distribution, not the underlying edge.

This is also why you should be careful with how you interpret the data. A higher at-least-one-pass rate does not mean the strategy became stronger. It means the account management process made failure less synchronized.

That is still valuable, especially if your priority is getting at least one funded account live.

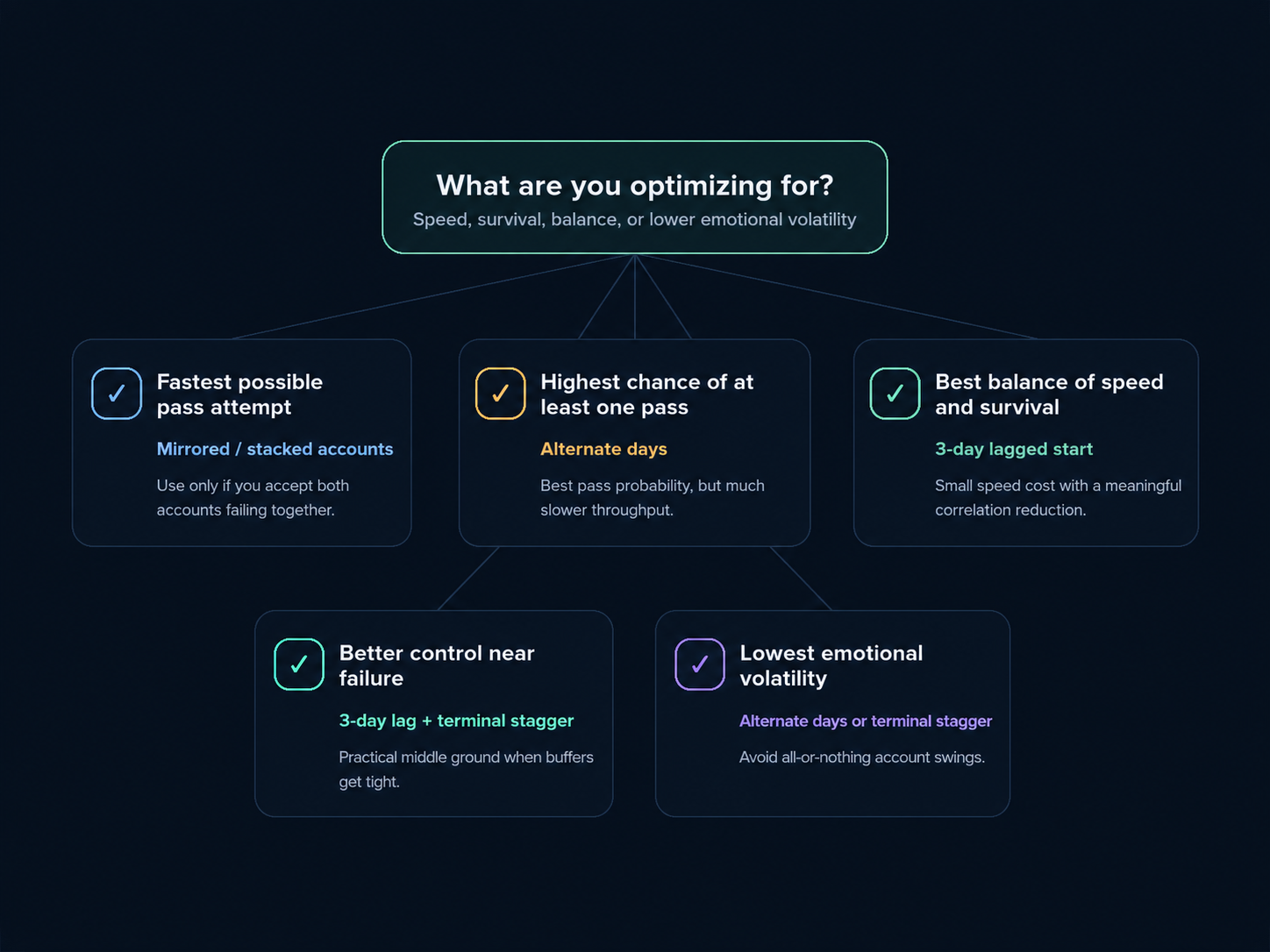

Which Prop Firm Account Rotation Strategy Should You Use?

There is no one-size-fits-all answer. The best prop firm account rotation strategy depends on your goals.

If you want maximum speed and you accept higher account correlation, stacked accounts are the fastest. Just understand that both accounts may fail together.

If your only goal is to maximize the chance of at least one pass, alternate days performed best in the test. It reached a 70.7% at-least-one-pass rate, but the average first pass day slowed to 17.6 opportunity days.

If you want a balanced approach, the 3-day lag is more practical. It improved the at-least-one-pass rate from 45.5% to 55.3%, with average first pass time barely moving from 9.7 to 10.2 opportunity days.

If you want the strongest middle-ground version, use a 3-day lag with terminal staggering. That pushed the at-least-one-pass rate to 61.6%, while keeping the average first pass day at 11.2 opportunity days.

A simple decision framework looks like this:

| Goal | Best Fit |

|---|---|

| Fastest possible pass attempt | Mirrored / stacked accounts |

| Highest chance of at least one pass | Alternate days |

| Best balance of speed and survival | 3-day lagged start |

| Better risk control near failure | 3-day lag + terminal stagger |

| Lowest emotional volatility | Alternate days or terminal stagger |

For most traders, the best starting point is the 3-day lag plus terminal stagger. It is simple, it reduces correlation, and it does not slow the process as much as full alternate-day rotation.

How to Build Your Own Account Rotation Rules

You do not need to copy these exact numbers blindly. Your strategy may behave differently.

A system with fewer trades, larger losses, or lower win rate may benefit from a different lag. A system with many small trades may handle rotation differently. A scalping strategy may need different rules than a swing strategy.

Here is a practical way to build your own rotation process:

- Define your valid trade setup.

- Decide how much risk each account gets per trade.

- Choose your starting rotation rule, such as a 3-day lag.

- Decide when an account becomes "terminal risk."

- Write down what happens when two accounts are terminal at the same time.

- Track account outcomes separately.

- Review pass rate, time to pass, fails, and account correlation.

The key is to make these decisions before you are under pressure. If you wait until an account is one loss away from failure, emotion will usually take over.

A written rule beats a last-minute decision.

Use Firm Rules to Improve the Setup Even More

Account rotation is only one part of the puzzle. The prop firm you choose also matters.

A strategy that works well with one firm's rules may struggle under another firm's drawdown model, profit target, payout rules, daily loss limits, or consistency requirements.

Before buying another evaluation, compare the rules across firms using the PropFirmWizard prop firm comparison database. This helps you find firms that better match your trading style instead of forcing your strategy into the wrong ruleset.

Then, use the PropFirmWizard prop firm pass rate calculator to estimate how different assumptions may affect your odds.

That combination is powerful:

- Use the comparison database to find better rules.

- Use the calculator to estimate your pass probability.

- Use account rotation to reduce correlation across multiple evaluations.

That is much smarter than buying two random challenges and hoping the trade sequence goes your way.

Common Mistakes Traders Make With Multiple Prop Firm Accounts

Multiple accounts can help you scale, but they can also expose bad habits faster. Watch out for these mistakes.

Copying Every Trade Without Thinking

Copy trading across accounts is not always wrong. The problem is doing it by default.

If every account has the same entry, same stop, same target, and same drawdown state, then all accounts are tied to the same outcome. That can be useful when you are trying to scale quickly, but it gives you less protection from a bad sequence.

Ignoring Account State

Two accounts can start the same, but they rarely stay the same.

One may be near the profit target. Another may be near max drawdown. Another may be flat. Treating all three accounts the same can lead to poor decisions.

A healthy account and a terminal-risk account should not always take the same trade.

Chasing the Highest Pass Rate Only

Alternate days had the highest chance of at least one pass in the test, but it was also the slowest pair-level method. If you care about throughput, you need to balance probability with time.

The best strategy is not just the one with the highest pass rate. It is the one that fits your goals, budget, patience, and trading frequency.

Switching Rules Mid-Challenge

Rotation only works if you follow the rules.

If you start with a lagged approach, then panic and copy everything after two wins, your results will not match the plan. The same goes for terminal staggering. The rule has to be defined before the account is under pressure.

Does This Apply to Funded Accounts Too?

Yes, the same logic can apply to funded accounts, but the stakes are different.

In an evaluation, the goal is to pass the challenge. In a funded account, the goal is to survive, withdraw, and scale over time.

That usually means you should be even more careful with correlation. Losing two evaluations at once hurts. Losing multiple funded accounts at once can be much worse.

For funded accounts, terminal staggering can be especially useful because payout eligibility, trailing drawdown, and account buffer can vary across accounts. An account with a large cushion may be able to take normal risk. An account close to a violation may need to sit out or trade smaller.

The basic question stays the same:

Do you want all accounts exposed to this same trade, or does it make more sense to spread the sequence?

A Simple Rotation Plan You Can Test

Here is a basic framework traders can test for two prop firm evaluations:

- Start Account A on the first valid opportunity.

- Start Account B three opportunity days later.

- Trade both accounts only when both have healthy drawdown buffer.

- If one account becomes terminal risk, prioritize that account by itself.

- If both accounts become terminal risk, trade only one on the next setup.

- Give the skipped account priority on the following valid setup.

- Reset the rotation after an account passes or fails.

This is not a promise that you will pass. No rotation rule can guarantee that.

But it gives you a structured process. Instead of making random decisions account by account, you are managing correlation on purpose.

That is a big step up from simply copying trades and hoping for the best.

Final Takeaway

Prop firm account rotation is not a magic trick. It will not turn a losing strategy into a winning one.

But if your strategy has an edge, rotation can help that edge survive bad sequencing.

In the Monte Carlo test, mirrored accounts had a 45.5% chance of at least one account passing. A 3-day lag raised that to 55.3%, while average first pass time barely moved from 9.7 to 10.2 opportunity days. Adding terminal staggering raised the at-least-one-pass rate again to 61.6%, with average first pass time at 11.2 days.

Alternate days produced the highest at-least-one-pass rate at 70.7%, but it was much slower at 17.6 average opportunity days to first pass.

So, the practical answer is this:

If you want the best balance between speed and survival, start with a lagged account approach and add terminal staggering when accounts get close to max drawdown.

Then, before buying the next challenge, run the numbers. Use the PropFirmWizard prop firm pass rate calculator to estimate your odds, and compare account rules with the PropFirmWizard prop firm comparison database.

Better firm selection, better account rotation, and better risk control can make a real difference.

FAQs

What is prop firm account rotation?

Prop firm account rotation is a method for deciding which account takes each trade when you are managing multiple evaluations or funded accounts. Instead of copying every trade across every account, you rotate exposure to reduce correlation and avoid losing multiple accounts on the same bad sequence.

Should I trade two prop firm evaluations at the same time?

You can, but it depends on your goal. Trading both accounts at the same time is faster when you win, but it also means both accounts can fail together. A lagged start or alternate-day approach may improve your chance of getting at least one account passed.

What is the best prop firm account rotation strategy?

In the research, alternate days had the highest chance of at least one account passing at 70.7%, but it was slower. The 3-day lag with terminal staggering was the strongest middle-ground approach, reaching a 61.6% at-least-one-pass rate with less delay.

What is terminal staggering?

Terminal staggering is a rule used when multiple accounts are close to failure. If two accounts are both in a "win-or-die" state, you trade only one of them on the next setup instead of risking both on the same trade.

Does account rotation improve my trading edge?

No. Account rotation does not improve your win rate, entries, exits, or expectancy. It changes how your trade sequence is distributed across accounts. The main benefit is reducing correlation between accounts.

How many days should I wait before starting the second prop firm account?

In the tested strategy, a 3-opportunity-day lag was a strong middle ground. Your ideal lag may be different depending on trade frequency, risk per trade, win rate, and drawdown rules.

Is alternate-day trading better for prop firm challenges?

Alternate-day trading can be better if your main goal is to maximize the chance of at least one account passing. In the test, it had the highest at-least-one-pass rate. The trade-off is that it took longer on average to get the first pass.

Can I use this strategy for funded accounts?

Yes. The same logic can apply to funded accounts, especially if you are managing multiple accounts with different drawdown buffers. In funded accounts, reducing correlation may be even more important because protecting payout eligibility matters.

How can I improve my prop firm challenge pass rate?

Start by choosing a firm with rules that match your strategy. Then estimate your odds with a pass rate calculator, reduce oversized risk, avoid over-correlating accounts, and use a written rotation plan before the challenge begins.